What is Shop Insurance?

Shop insurance is a specialized type of business insurance designed to protect retail shop owners like you against various risks, including property damage, theft, liability claims, and business interruptions. It’s essentially your safety net—a way to prepare for the unexpected so you can focus on running your shop with peace of mind.

Key Components of Shop Insurance:

- Property Insurance: Covers damages to the shop’s building and contents due to fires, floods, or vandalism. Imagine if a storm damages your storefront—this type of coverage ensures repairs don’t come out of your pocket.

- Liability Insurance: Protects against third-party claims arising from injuries or damages caused within the shop premises. If a customer slips and falls in your shop, liability insurance can cover medical bills and legal fees.

- Business Interruption Insurance: Compensates for lost income during periods when your shop cannot operate, like after a fire or major repair.

- Employee Coverage: Ensures workers are protected in case of workplace injuries or illnesses, which can also protect you from lawsuits.

When you think about shop insurance, think of it as a customized shield against the various risks that come with running a business.

Before, jump into the detailed thourough explanation of shop insurance, let's try to understand the most dangerous risks associated with shops running without a shop insurance.

Risks of Running a Shop Without Insurance

Let’s be honest, running a shop without insurance is like walking a tightrope without a safety net. It exposes you to a variety of risks, some of which can be financially and emotionally devastating. Here are some risks you might face.

But, first, let's have a look at the recent data.

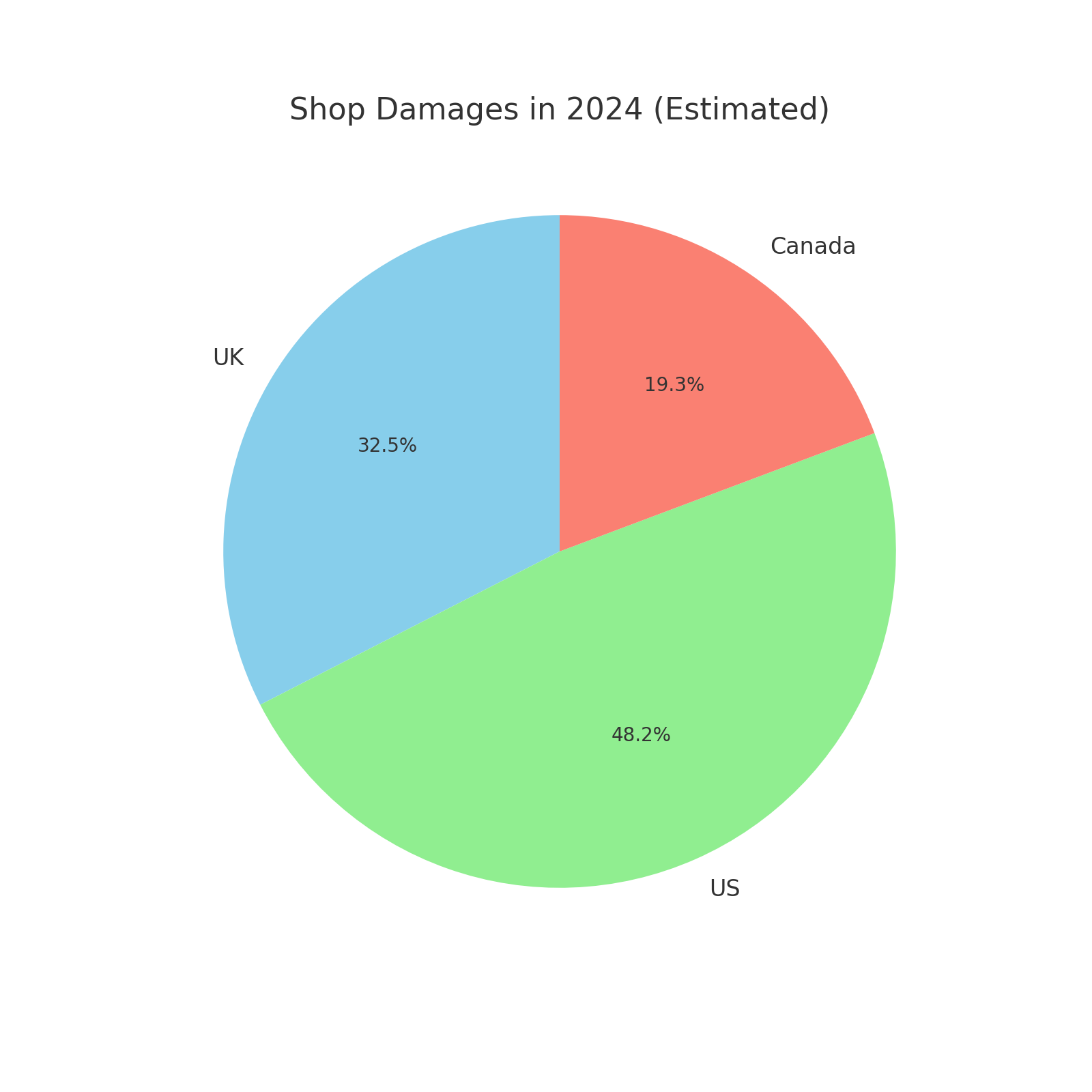

The pie chart illustrates the estimated shop damages in 2024 across three countries: the UK, US, and Canada. The UK accounted for 33.8% of the total damages, with approximately 13,500 shop closures, largely influenced by economic challenges and high operational costs.

The US experienced the highest share, at 50.1%, with around 20,000 shop damages, driven by natural disasters and shifting retail trends.

Canada contributed 16.1%, with approximately 8,000 damages, highlighting vulnerabilities in smaller retail sectors. This data emphasizes the growing need for shop insurance worldwide.

There are multiple reasons causing damages to shops. Few of them have discussed below.

- Natural Disasters: Think about hurricanes, earthquakes, or floods. These events can destroy your shop’s physical structure and inventory, leaving you with enormous out-of-pocket expenses. For example, a small shop in Florida faced total destruction during Hurricane Ian, and without insurance, the owner had to close permanently due to financial inability to rebuild.

- Cybersecurity Threats: In today’s digital age, even small shops can fall victim to data breaches or ransomware attacks. Cybercriminals can steal sensitive customer or financial data, resulting in hefty fines and reputational damage. Without cyber liability insurance, you’d need to bear the cost of legal battles and recovery services, which could easily reach tens of thousands of dollars.

- Employee-Related Issues: Workplace injuries or legal disputes with employees can lead to unexpected expenses, which insurance can help cover. Imagine if an employee slips in your storage area and suffers a serious injury. Without worker’s compensation insurance, you might have to cover medical costs and lost wages out of pocket while potentially facing legal action.

- Financial Losses: Imagine a fire or theft wiping out your inventory. Without insurance, you’d be responsible for replacing everything out of your own pocket. For instance, a shop in California experienced losses worth $50,000 after a break-in, which took years to recover without insurance.

- Legal Penalties: Many states require businesses to have certain types of insurance. If you’re caught operating without it, you could face fines or even closure. For example, failing to have liability insurance could result in penalties ranging from $500 to several thousand dollars, depending on the state.

- Reputation Damage: If you can’t handle incidents responsibly, customers may lose trust in your business. Imagine a scenario where a customer sues you for injury, and you can’t afford to pay the settlement. News spreads fast, and potential customers might avoid your shop altogether.

- Operational Downtime: Recovering from a disaster can take time. Without insurance, it might take much longer—or worse, you might never recover at all. For example, after a fire, uninsured businesses often struggle to secure funds for rebuilding, forcing them to shut down for extended periods or permanently.

I always say, it’s not about expecting the worst but being ready for it. Don’t let one unfortunate event derail your dreams.

How Shop Insurance Promotes Business Growth ?

Running a shop—whether it’s in the U.S., Canada, or the U.K.—isn’t just about selling products. It’s about building trust, ensuring financial stability, and paving the way for future success. As a shop owner, you might not always think about the “what ifs,” but having shop insurance can make a world of difference, especially when it comes to growing your business. Let’s break it down and see how shop insurance helps your business thrive.

1. Gaining Customer Trust

Think about it—would you shop at a place that feels unprofessional or unprepared for emergencies? Customers want to know they’re in safe hands. Having shop insurance shows that you care about their safety and your business’s stability. For example, liability insurance ensures that if a customer slips and falls in your shop, you can cover their medical expenses without going bankrupt. This kind of preparedness builds trust, and trust is what brings customers back and encourages them to recommend your shop to others.

2. Meeting Legal and Lease Requirements

Did you know that many landlords and governments require shop insurance? In the U.S. and Canada, landlords often ask for property or liability coverage before you can rent a space. Similarly, in the U.K., businesses are legally required to have employer’s liability insurance if they hire staff. By staying compliant, you avoid legal troubles that could distract you from growing your shop. Plus, fulfilling these requirements makes it easier to expand your business into new locations or markets.

3. Protecting Your Finances During Crises

Life happens, and sometimes it’s not pretty. A fire, theft, or even a flood can cause serious damage to your shop. Without insurance, the costs to repair or restock can drain your savings—or worse, force you to shut down. With shop insurance, you’re protected. For instance, a small bookstore in Canada bounced back within weeks after a fire because their insurance covered both repairs and lost revenue. This financial safety net ensures you can recover and keep moving forward.

4. Supporting Your Expansion Plans

When you know you’re covered for unexpected issues, you can take bigger, bolder steps to grow your business. Whether you’re adding a second location, expanding your product line, or going online, insurance gives you the peace of mind to focus on your goals. For example, a café owner in London used their comprehensive insurance policy to confidently invest in a second branch, knowing potential risks like equipment breakdowns were covered.

5. Preserving Your Reputation

Imagine this: A flood damages your shop, and you don’t have insurance. Customers see you struggling to recover, and your reputation takes a hit. On the other hand, with shop insurance, you can handle emergencies professionally and quickly. This resilience leaves a lasting impression on your customers, employees, and even your suppliers. A strong reputation doesn’t just attract more customers—it also opens doors to partnerships and other growth opportunities.

6. Building a Resilient Business

At the end of the day, shop insurance isn’t just about avoiding disasters—it’s about building a foundation for growth. Whether you’re in New York, Toronto, or Manchester, the challenges shop owners face are similar, and having insurance is a key part of staying competitive.

So, if you’re looking to grow your shop, don’t just focus on profits and expansion plans—make sure you’re protected. By investing in shop insurance, you’re not just safeguarding what you’ve built; you’re creating the freedom and security to aim even higher. After all, growth starts with stability, and stability starts with being prepared.

Why Shop Insurance Is Important for Small Businesses

Running a small business is no small feat. Whether you're managing a boutique, a coffee shop, or a convenience store, you’ve poured your heart, time, and resources into making your dream a reality. But have you considered how vulnerable your shop might be without insurance? If you're a small business owner in the U.S., Canada, or the U.K., shop insurance isn’t just a safety net—it’s a necessity. Let’s explore why having shop insurance is critical for small businesses like yours.

1. Protecting Your Investment

As a small business owner, your shop is likely one of your biggest investments. From the inventory to the equipment, everything you own contributes to your livelihood. But what happens if there’s a fire, a flood, or a burglary?

For example, a small clothing store in Toronto faced over $20,000 in losses after a break-in. Without insurance, that shop would have had to shut down. With shop insurance, you’re covered for damages and losses, so you can recover and get back to business faster.

2. Shielding You From Legal Risks

One unexpected lawsuit could devastate a small business. Whether it’s a customer who slips and falls or a supplier dispute, legal fees can pile up quickly. Liability insurance protects you from these risks by covering medical expenses, legal costs, and potential settlements.

In the U.K., it’s a legal requirement for businesses with employees to have employer’s liability insurance. If you fail to comply, you could face fines of up to £2,500 per day! Having the right insurance not only protects your business but also ensures you’re staying on the right side of the law.

3. Ensuring Business Continuity

When disasters strike, small businesses often lack the financial buffer that larger companies have. That’s why business interruption insurance is a lifesaver. Imagine your shop is forced to close for repairs after a natural disaster. This coverage ensures you can still pay your rent, utilities, and employee salaries while your shop is out of action.

For instance, a bakery in Florida was able to survive three months of closure after a hurricane, thanks to their business interruption insurance. Without it, they would’ve been bankrupt.

4. Helps Gaining Customer and Vendor Trust

Insurance isn’t just about protection—it’s also about credibility. Being insured tells your customers, suppliers, and partners that you take your business seriously.

For example, if you’re working with a major vendor, they may require proof of insurance before signing a contract with you. Similarly, customers feel reassured knowing they’re dealing with a responsible business. This trust can lead to repeat business and long-term growth.

5. Managing Employee-Related Risks

If you have employees, you have a responsibility to ensure their safety. Workplace injuries can lead to significant costs, especially if you don’t have workers’ compensation insurance. In the U.S., for example, failing to carry workers’ compensation can result in hefty fines or even legal action. Workers’ comp doesn’t just protect your employees; it protects your business from financial and legal troubles that could arise from workplace incidents.

6. Affordable Protection for Small Budgets

One of the biggest myths about shop insurance is that it’s expensive. The truth is, many insurance providers offer policies specifically tailored to small businesses. Whether you’re in New York, Vancouver, or Manchester, you can find coverage that fits your budget without compromising on protection.

Think of it this way: a small monthly premium is a small price to pay compared to the financial fallout of an uninsured disaster.

7. Safeguarding Against Everyday Risks

It’s not just the big disasters you need to worry about. Everyday risks—like a power surge damaging your equipment or a minor accident in your shop—can also lead to unexpected expenses. With the right insurance, you’re covered for these smaller but frequent risks, ensuring that they don’t snowball into bigger financial issues.

Who Should Buy Shop Insurance?

Shop insurance is essential if you want to protect your business. It’s not just for large stores or malls. Many shop owners benefit from it. Let me tell you who should definitely consider shop insurance and why it’s so important.

- Retail Store Owners: If you own a retail store, you deal with customers daily. Accidents like slips or damaged products can happen anytime.

Shop insurance covers you against such risks.

For example, in 2023, many shop owners in the U.S. faced claims for customer injuries. Imagine how helpful insurance could be for handling those unexpected costs. It’s better to invest in shop insurance than to pay huge bills later. - Café or Restaurant Owners: Running a café or restaurant means handling food, drinks, and a lot of foot traffic. A spilled drink or kitchen fire could lead to big losses. Shop insurance ensures you can recover without shutting down your business. In fact, research shows that over 50% of food businesses in the UK in 2024 had claims for property damage. Don’t you think it’s wise to have insurance that protects your livelihood?

- Small Business Owners: Even if you run a small shop, you still need shop insurance. Theft, natural disasters,

or lawsuits don’t discriminate based on shop size. For instance, in 2024, small businesses in India reported a significant rise in

theft cases.

Shop insurance helps you recover losses and stay stress-free. Why leave your shop unprotected when affordable options are available? - Online Store Owners with Warehouses: Do you own an online store and use a warehouse for storage? Shop insurance is for you too. It covers stock damage caused by fire, floods, or theft. In 2023, warehouses in California faced heavy losses due to floods. Think about how much easier it would be if you had insurance to cover such damages.

- Flower Shop Owners: If you own a flower shop, your stock is highly perishable and sensitive to

conditions like temperature and humidity. Unexpected events such as refrigeration failure, theft, or fire can lead to significant losses.

Coffee shop or café owners face unique risks, from equipment breakdown to liability issues due to hot beverages. Imagine a coffee machine malfunctioning during peak hours or a customer spilling a drink and getting injured. Shop insurance provides coverage for such incidents, ensuring your business can keep running smoothly.

Read complete detail of- Flower Shop Insurance

In short, shop insurance isn’t just a luxury. It’s a necessity for anyone who owns a business. Whether you run a retail store, café, small shop, or online store, shop insurance gives you peace of mind.

If you're a small cafe or restaurant owner or running a retail store at countryside, buying a shop insurance is highly recommended. If you're still not convinced or required more details, keep reading below. You'll definitely find a strong reason why you should consider it and why not?

Why You Should Buy a Shop Insurance?

As a shop owner, you pour your heart, time, and resources into running your business. But no matter how prepared you are, unexpected situations can disrupt your operations and threaten your livelihood. That’s where shop insurance steps in. Let me walk you through the key benefits of buying shop insurance and why it’s a must-have for every shop owner like you.

1. Protection Against Property Damage

Imagine this: a fire breaks out or a severe storm damages your storefront. Without shop insurance, the cost of repairs could be devastating. Shop insurance covers property damage, including your building, equipment, and inventory. It ensures that you won’t have to dig deep into your savings—or worse, shut down your business—because of an unforeseen disaster.

2. Coverage for Theft and Vandalism

Theft and vandalism are risks no shop owner can ignore. If someone breaks into your store or vandalizes your property, the financial loss could be overwhelming. With shop insurance, you’re covered for stolen goods and the cost of repairs, giving you peace of mind knowing you can recover quickly.

4. Business Continuity During Interruptions

Let’s say a burst pipe floods your store and forces you to close temporarily. Without income, how will you pay rent, salaries, or bills? Shop insurance often includes business interruption coverage, which compensates you for lost income during downtime. It keeps your business afloat until you can reopen.

In fact, during the 2021 Texas winter storm, a small grocery store owner used their shop insurance to recover after a burst pipe destroyed thousands of dollars' worth of inventory. The policy not only reimbursed the losses but also helped cover rent during the closure.

5. Peace of Mind for You

Owning a shop comes with plenty of stress, but insurance allows you to focus on running your business without constant worry about potential risks. Knowing you’re prepared for any curveball life throws at you gives you the confidence to grow and succeed.

Investing in shop insurance isn’t just a smart financial decision; it’s a commitment to your business’s long-term stability. Don’t wait for disaster to strike—protect what you’ve worked so hard to build today.

Benefits of Shop Insurance

Shop insurance is one of the most important investments you can make for your business. Whether you run a small boutique or a large retail store, having the right shop insurance can protect you from unexpected losses. In this section, we will explore the key benefits of having shop insurance and why it’s essential for your business’s success.

1. Protects Your Property

One of the primary benefits of shop insurance is the protection it provides for your business property. Whether it's the physical structure of your shop, your inventory, or your equipment, shop insurance ensures that you're covered in case of damage or loss. For example, if a fire breaks out or a storm damages your store, your insurance can help you repair or replace the affected property.

- Property Damage Coverage: Covers damage to your shop building, stock, and equipment due to fire, theft, or natural disasters.

- Theft Protection: If your shop is broken into, insurance can cover the loss of goods and property.

2. Liability Protection

As a shop owner, you’re responsible for the safety of your customers and employees. Shop insurance provides liability coverage to protect you against legal claims made by third parties. This is particularly important if someone gets injured while on your premises. For instance, if a customer slips on a wet floor in your store and files a lawsuit, liability coverage can help cover legal fees and compensation costs.

- General Liability Insurance: Protects you against third-party claims for injury or property damage on your premises.

- Product Liability Insurance: Covers any damages caused by products sold in your shop.

3. Business Interruption Coverage

What happens if your business is forced to close temporarily due to a covered event, such as a fire or flood? Business interruption insurance comes into play here. It helps replace lost income while your shop is closed for repairs. Without this coverage, you could struggle to cover ongoing expenses like rent, salaries, and utilities during the downtime.

- Financial Support During Downtime: Helps replace lost income when your shop is unable to operate.

- Continuing Overheads: Covers fixed costs such as rent and wages while your shop is closed for repairs.

4. Employee Protection

If you have employees, shop insurance can also protect them. Workers' compensation insurance is a common addition to shop insurance policies. It provides coverage for your employees if they get injured or fall ill while working. For example, if a delivery driver injures themselves while unloading stock, workers' compensation insurance will cover their medical bills and lost wages.

- Medical Coverage: Pays for medical expenses for employees injured at work.

- Lost Wages: Provides financial support if an employee is unable to work due to an injury.

5. Peace of Mind

Running a business can be stressful, especially when unexpected events occur. Shop insurance offers peace of mind, knowing that you're covered if something goes wrong. Whether it's a fire, theft, or a legal claim, having insurance allows you to focus on growing your business without constantly worrying about potential risks. For example, knowing that you're covered for property damage can allow you to focus on improving your product offerings instead of stressing over worst-case scenarios.

- Financial Security: Protects your business from significant financial losses due to unforeseen events.

- Reduced Stress: Allows you to run your business without constant worry about risks.

6. Customizable Coverage

Shop insurance is not a one-size-fits-all solution. You can customize your policy based on the specific needs of your business. Whether you need additional coverage for expensive equipment, or extra protection against product liability, most insurance providers offer add-ons that allow you to tailor your policy. This means you can get exactly what you need, without paying for unnecessary coverage.

- Tailored Policies: Customize your coverage to fit your shop's unique needs.

- Additional Coverage Options: Add extra coverage for specific risks such as equipment breakdowns or cyberattacks.

7. Helps Build Your Business Reputation

Having shop insurance also enhances your business's credibility. Customers and suppliers often view businesses with insurance as more reliable and professional. It shows that you're serious about protecting your business and your customers. For example, if you have liability coverage, customers will feel more confident knowing that they’re protected if something goes wrong on your premises.

- Trust and Credibility: Customers feel more confident knowing your business is insured.

- Supplier Confidence: Suppliers may prefer to work with businesses that have adequate insurance coverage.

Types of Shop Insurance

Shop insurance is a crucial consideration for any business owner, offering protection against a variety of risks that could impact the operation of the shop. While the exact types of coverage may vary slightly between countries such as the U.S., U.K., and Canada, the core types of shop insurance are generally similar. Below are the main types of shop insurance that are essential for businesses across these regions:

1. General Liability Insurance

General Liability Insurance is fundamental for any retail business. It covers legal and compensation costs if someone is injured on your premises or if your business causes damage to third-party property. This is one of the most basic and necessary insurance types for shop owners to protect against potential claims from customers or the public.

For Example:- If a customer slips on a wet floor in your shop and files a lawsuit for their injuries, General Liability Insurance would cover the legal costs and any compensation payments required.

2. Commercial Property Insurance

This type of insurance covers damage to your shop’s physical assets, including the building (if owned) and its contents, such as inventory, equipment, and furniture. It protects against risks like fire, theft, vandalism, or natural disasters.

Example: If a fire breaks out and destroys your inventory, Commercial Property Insurance would reimburse you for the cost of replacing the damaged goods and repairing the shop.

3. Employer's Liability Insurance

In countries like the U.S. and Canada, Employer’s Liability Insurance (often part of workers' compensation insurance) is a legal requirement if you employ staff. It covers the legal and compensation costs if an employee becomes injured or ill due to their work.

Example: If an employee sustains a back injury while lifting heavy boxes in your shop, Employer's Liability Insurance will cover medical expenses and any legal fees related to the incident.

4. Business Interruption Insurance

Business Interruption Insurance helps protect against loss of income if your business is temporarily closed due to an unexpected event, such as a fire, flood, or other disasters. It can cover lost revenue and ongoing expenses like rent and staff salaries during the recovery period.

Example: If a flood damages your shop and forces you to shut down for repairs, Business Interruption Insurance would cover the loss of income during the closure period.

5. Product Liability Insurance

For shops selling physical goods, Product Liability Insurance is essential. It protects against claims arising from injury or damage caused by products sold by your business. This type of coverage ensures that you are protected in case a product malfunctions or causes harm to a customer.

Example: If a customer is injured by a defective product purchased from your shop, Product Liability Insurance would cover the legal and compensation costs.

6. Stock Insurance

Stock Insurance protects the goods or merchandise you sell. This type of policy covers the cost of replacing stolen, damaged, or lost stock, ensuring that you can continue trading without incurring a significant financial loss due to inventory depletion.

Example: If your shop is broken into and a large portion of your stock is stolen, Stock Insurance would reimburse you for the lost inventory, enabling you to restock your shelves.

7. Cyber Liability Insurance

As e-commerce grows and businesses handle more sensitive customer data, Cyber Liability Insurance has become increasingly important. It covers the costs of data breaches, cyberattacks, and other online security threats, including legal fees and customer notification costs.

Example: If your online store is hacked and customer data is compromised, Cyber Liability Insurance would cover the costs associated with resolving the breach, including legal fees, customer compensation, and data recovery.

8. Workers' Compensation Insurance

While often bundled with Employer's Liability Insurance in some regions, Workers’ Compensation Insurance is a standalone coverage in others. It provides compensation for employees who suffer work-related injuries or illnesses, covering medical expenses and lost wages. It is a legal requirement in many countries for businesses with employees.

Example: If an employee is injured while operating machinery in your store, Workers' Compensation Insurance would cover their medical treatment and rehabilitation expenses.

9. Commercial Auto Insurance

If your business owns vehicles or uses them for deliveries or other operations, Commercial Auto Insurance is necessary. It covers the vehicle, driver, and any associated liabilities in case of an accident.

Example: If your delivery vehicle is involved in an accident while delivering goods to a customer, Commercial Auto Insurance would cover the damage to the vehicle and any liability for injuries or damages caused.

How to Choose the Right Shop Insurance Policy

Choosing the right shop insurance policy is essential for protecting your business. Whether you run a small retail shop or a large store, the right coverage can save you from financial losses caused by unexpected events. In this guide, we’ll walk you through the steps to help you select the best shop insurance policy for your needs.

1. Assess Your Shop's Risk

Before purchasing shop insurance, you need to assess the risks your shop faces. Understanding the specific risks involved in your business will help you choose the right coverage. For example:

- Does your shop face risks related to theft, fire, or vandalism?

- Do you operate in an area prone to natural disasters?

- Do you have valuable equipment or stock that requires special protection?

Identifying these risks is the first step in choosing the right policy. Once you know your risks, you can look for an insurance policy that covers them adequately.

2. Understand the Different Types of Shop Insurance

There are several types of shop insurance available, and each type covers different aspects of your business. Here are the key types to consider:

- Property Insurance: This covers damages to your shop and inventory due to events like fire, theft, or natural disasters.

- Liability Insurance: This protects you against claims made by customers or third parties for injury or damage that occurs in your shop.

- Business Interruption Insurance: This helps replace lost income if your shop is forced to close due to a covered event, such as a fire or flood.

- Employee Insurance: If you have employees, this provides coverage for their injuries or illnesses while working.

Understanding the different types of shop insurance policies will help you select the coverage that best fits your business needs.

3. Compare Policies from Different Insurers

Not all insurance companies offer the same policies or premiums. It's important to compare policies from multiple insurers to ensure you're getting the best deal. Here’s what you should look for when comparing shop insurance policies:

- Coverage Limits: Check if the coverage limits meet your business requirements.

- Exclusions: Review the policy’s exclusions to understand what’s not covered.

- Premium Rates: Compare the premiums to ensure they’re within your budget.

- Claims Process: Understand how easy it is to file a claim and whether the insurer has a good reputation for handling claims.

By comparing these factors, you’ll be able to choose a policy that offers the best value for your money.

4. Customize Your Policy to Fit Your Needs

Every shop is unique, so you may need to customize your shop insurance policy. Many insurers offer add-ons or riders that you can use to tailor the coverage to your business. Some common add-ons include:

- Theft Protection: If you have valuable stock or equipment, consider adding theft protection to your policy.

- Equipment Breakdown: If you rely on machinery or equipment, this add-on can protect you from costly repairs or replacements.

- Business Auto Insurance: If your business involves transportation or delivery, you may need business auto coverage in addition to standard shop insurance.

By customizing your policy, you ensure that all aspects of your shop are protected.

5. Check the Insurer’s Reputation

Choosing a reputable insurer is crucial. A good insurance company will offer reliable customer service, prompt claims processing, and transparent policy terms. Before making your decision, research the insurer’s reputation:

- Read online reviews and ratings from other customers.

- Check the insurer's financial stability to ensure they can pay out claims when needed.

- Ask other business owners for recommendations on insurers they trust.

By choosing a reputable insurer, you can have peace of mind knowing that your shop is in good hands.

6. Review Your Policy Regularly

Your shop’s needs may change over time, so it’s important to review your insurance policy regularly. As your business grows or changes, you may need to adjust your coverage to ensure it continues to meet your needs. Consider reviewing your policy annually or whenever there’s a major change in your business operations.

Factors Affecting Shop Insurance Premiums

When you purchase shop insurance, one of the most important things to consider is the premium you'll need to pay. Insurance premiums can vary widely depending on several factors. Understanding these factors can help you make better decisions when selecting a policy. In this section, we’ll break down the key factors that influence shop insurance premiums and how they can impact your costs.

1. Location of Your Shop

The location of your shop plays a significant role in determining your insurance premium. If your shop is located in an area prone to natural disasters, such as floods or earthquakes, your premium will likely be higher. For example, if your shop is in a flood-prone area, your insurer may increase your premium to cover potential water damage.

- Flood Zones: Areas prone to flooding may lead to higher premiums due to the risk of water damage.

- Urban vs Rural: Shops in busy urban areas with higher crime rates may also face higher premiums.

2. Type of Business

The type of business you operate directly affects your shop insurance premium. Businesses with higher risks, such as those involving hazardous materials, machinery, or large amounts of inventory, will generally pay higher premiums. For instance, a shop selling flammable materials or electronics may have higher insurance premiums compared to a clothing store.

- Riskier Products: Shops dealing with hazardous items, like chemicals, face higher premiums.

- Inventory Size: Large stores with a high volume of inventory may pay higher premiums for property coverage.

3. Coverage Amount and Deductibles

The amount of coverage you choose and your deductible (the amount you pay out of pocket before insurance kicks in) can also impact your premiums. Higher coverage limits typically result in higher premiums, as you're asking the insurer to cover more risk. On the other hand, choosing a higher deductible can lower your premium, but it means you'll have to pay more if you need to file a claim.

- Higher Coverage: Opting for higher coverage limits will lead to higher premiums.

- Higher Deductibles: Choosing a higher deductible can help reduce your premium but increases your financial responsibility during a claim.

4. Security Features of Your Shop

If your shop has strong security measures in place, such as surveillance cameras, alarm systems, or fire suppression systems, it can lower your insurance premium. Insurance providers view these features as risk-reducing measures, meaning they’re less likely to have to pay out claims. For example, a shop with a top-tier security system will likely pay lower premiums than a shop without one.

- Surveillance Systems: Shops with security cameras can receive discounts on premiums.

- Fire Protection: Fire alarms and sprinklers can lower premiums by reducing the risk of fire damage.

5. Claims History

Your shop’s claims history is another important factor. If your shop has made multiple claims in the past, insurers may see your business as a higher risk and increase your premiums. Conversely, a shop with no claims history may be eligible for lower rates. Insurance providers often offer discounts to businesses with a clean claims record as they are considered less risky.

- Frequent Claims: A history of frequent claims can raise your premiums due to perceived risk.

- No Claims: Shops with a clean claims record may qualify for lower premiums.

6. Shop's Size and Structure

The size and structure of your shop can also influence your insurance premium. Larger shops generally have higher premiums because they present a greater risk in terms of property damage, theft, or liability. Additionally, the materials used to build your shop can impact premiums. For example, a brick-and-mortar shop may be cheaper to insure than one made of wood, which is more vulnerable to fire.

- Size of Shop: Larger shops with more square footage often incur higher premiums due to increased risk.

- Building Materials: Buildings made of fire-resistant materials can lower your premiums.

7. Business Revenue and Employee Count

The revenue your shop generates and the number of employees you have can also affect your premium. Higher revenue and more employees typically lead to higher premiums because they increase the insurer’s risk. A high-revenue business with many employees may face higher liability risks, so the premium will reflect that.

- High Revenue: Larger businesses with higher revenue may face higher premiums due to the increased risk.

- More Employees: A larger workforce increases the liability risk, which can lead to higher premiums.

Common Myths About Shop Insurance

When it comes to shop insurance, there are several misconceptions that can make business owners hesitate to get the coverage they need. These myths can lead to costly mistakes, so it's important to set the record straight. In this section, I’ll address some of the most common myths about shop insurance and explain the reality behind them.

1. Shop Insurance Is Only for Large Businesses

A lot of shop owners believe that only large businesses need insurance. But this isn't true. Whether you have a small local shop or a larger store, insurance is vital for protecting your business from risks like theft, fire, or damage. For example, even a small coffee shop could suffer a significant financial loss if it faces a break-in or a fire without proper coverage.

- Myth: Only big businesses need shop insurance.

- Fact: Small businesses need insurance too, as it protects against unexpected risks like property damage or theft.

2. Shop Insurance Covers Everything Automatically

Another common misconception is that shop insurance automatically covers every type of risk. The truth is, no policy is all-encompassing. There are exclusions in most policies, such as wear and tear or certain natural disasters. It’s important to review your policy and understand what’s covered to avoid surprises later on.

- Myth: Shop insurance covers all types of damage.

- Fact: Shop insurance has exclusions, so it’s essential to review the policy and add any necessary coverage for specific risks.

3. Shop Insurance Is Too Expensive

Many business owners think shop insurance is too expensive and avoid getting it. However, the cost of insurance can actually be quite affordable, especially if you tailor it to your needs. The price of not having insurance could be much higher if something unexpected happens, such as a major loss or lawsuit.

- Myth: Shop insurance is expensive and not worth the cost.

- Fact: Shop insurance can be affordable and is a small price to pay for protecting your business from costly risks.

4. Shop Insurance Automatically Covers Employee Injuries

Some shop owners mistakenly think that shop insurance includes coverage for employee injuries. However, shop insurance usually does not cover work-related injuries. For this, you will need separate workers’ compensation insurance, which helps cover medical expenses and lost wages for employees injured on the job.

- Myth: Shop insurance covers employee injuries automatically.

- Fact: Employee injuries are typically covered by workers’ compensation insurance, not shop insurance.

5. Shop Insurance Only Covers Property Damage

Many believe that shop insurance only protects against physical damage to property. While property coverage is a key part of shop insurance, it often includes other types of protection too, like liability coverage, business interruption, and even cyberattack protection. These additional coverages help ensure your business is well-protected against a wide range of risks.

- Myth: Shop insurance only covers property damage.

- Fact: Shop insurance can also cover liability, business interruptions, and even cyber-related risks.

Technical Terms Used in Shop Insurance

- Premium - The amount of money you pay for your insurance policy. Insurance premium typically paid monthly, quarterly, or annually to maintain coverage.

- Coverage - The types of risks or perils that the insurance policy protects against. This can include fire, theft, and vandalism among others.

- Deductible - The amount you must pay out of pocket before the insurance company begins to cover the claim. A higher deductible generally lowers your premium.

- Liability Insurance - A coverage option that protects against legal claims resulting from injuries or damages that occur on your business premises.

- Exclusions - Specific risks or circumstances that are not covered by the insurance policy. It is important to review these to understand what your policy does not protect against.

- Claim - A formal request made by the policyholder to the insurance company for compensation after a covered event occurs, like property damage or loss.

- Underwriting - The process by which an insurer evaluates the risk and decides the terms of the policy, including the premium and coverage levels.

- Endorsement - A written document attached to the insurance policy that modifies or adds coverage, such as increasing coverage limits or adding new items.

- Policyholder - The person or business that owns the insurance policy and is entitled to receive coverage in case of a claim.

- Replacement Cost - The amount needed to replace or repair damaged property with materials of similar kind and quality, without deducting for depreciation.

Shop Insurance FAQs

1. What is shop insurance, and why do I need it?

2. What does a shop insurance policy cover?

3. Can shop insurance cover theft or burglary?

4. How much does shop insurance cost?

5. Are natural disasters covered by shop insurance?

6. Can I customize my shop insurance policy?

7. Do I need shop insurance for a rented space?

8. Does shop insurance cover employee injuries?

9. Does shop insurance cover business interruption?

10. How do I choose the right shop insurance policy?

11. Can I add extra coverage to my shop insurance policy?

12. Is shop insurance mandatory for all businesses?

13. What documents are required for shop insurance claims?

14. How quickly are shop insurance claims settled?

15. Can I cancel my shop insurance policy anytime?

16. What is public liability in shop insurance?

17. Can shop insurance cover fire accidents?

18. Is there a deductible in shop insurance policies?

19. Can I renew my shop insurance policy online?

20. Does shop insurance cover temporary closures?

** About InsuranceBolo

Our blog is dedicated to educating insurance buyers with unbiased, simplified, and expert information. We focus on empowering individuals with detailed insights across various insurance categories, without selling policies or promoting providers. With a "no-call, no-sales" policy, we ensure a pressure-free experience for our readers.

We cover key insurance categories like Mobile Insurance, Cargo Insurance, and Term Life Insurance, providing clear and actionable information.

Take Action Today

Explore our expert guides and compare policies to simplify your insurance journey with confidence!